We’ve been hard at work developing a new email matrix in order to better improve our onboarding experience, and (hopefully) broaden relationships with our indirect Members.

Responsible for overall creative direction.

Sound strategy. Canny creative.

We’ve been hard at work developing a new email matrix in order to better improve our onboarding experience, and (hopefully) broaden relationships with our indirect Members.

Responsible for overall creative direction.

News Before & After

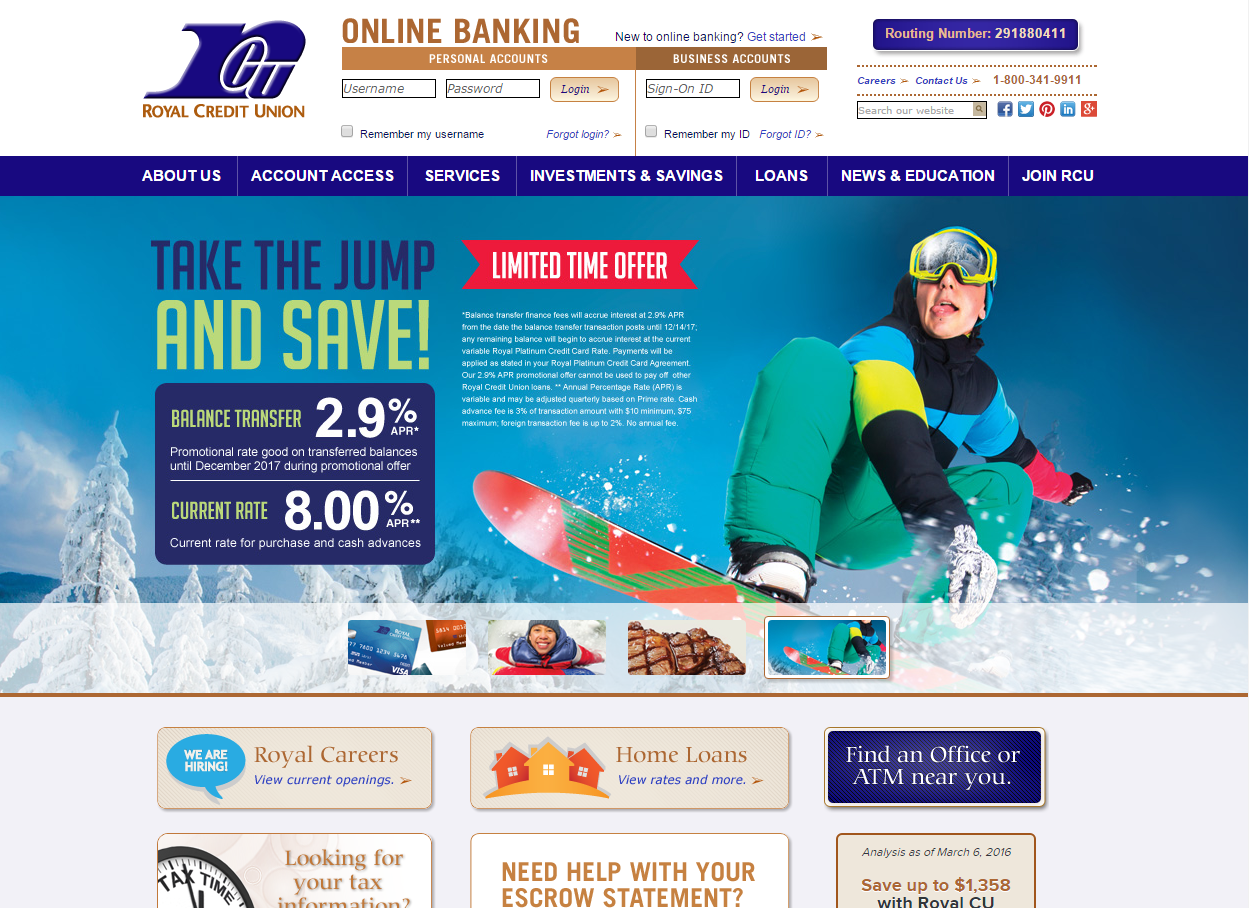

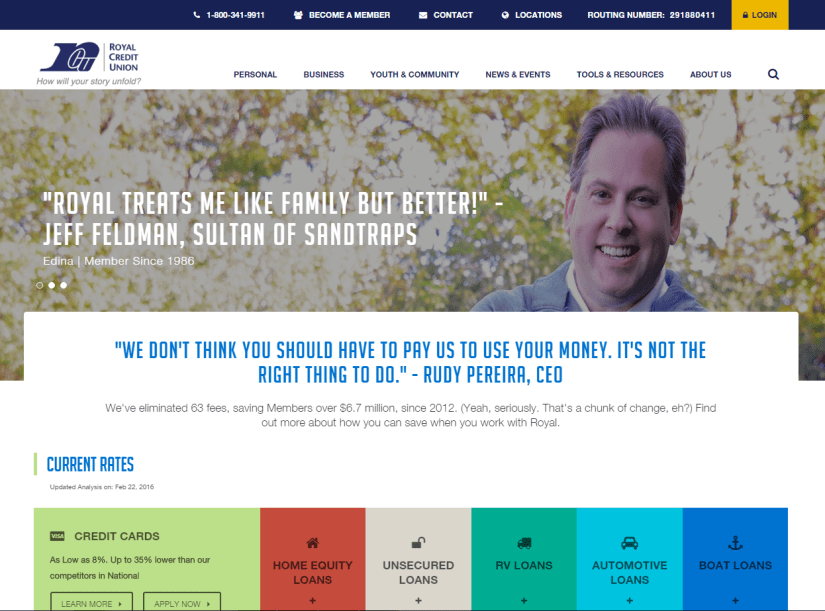

Home Page Before & After

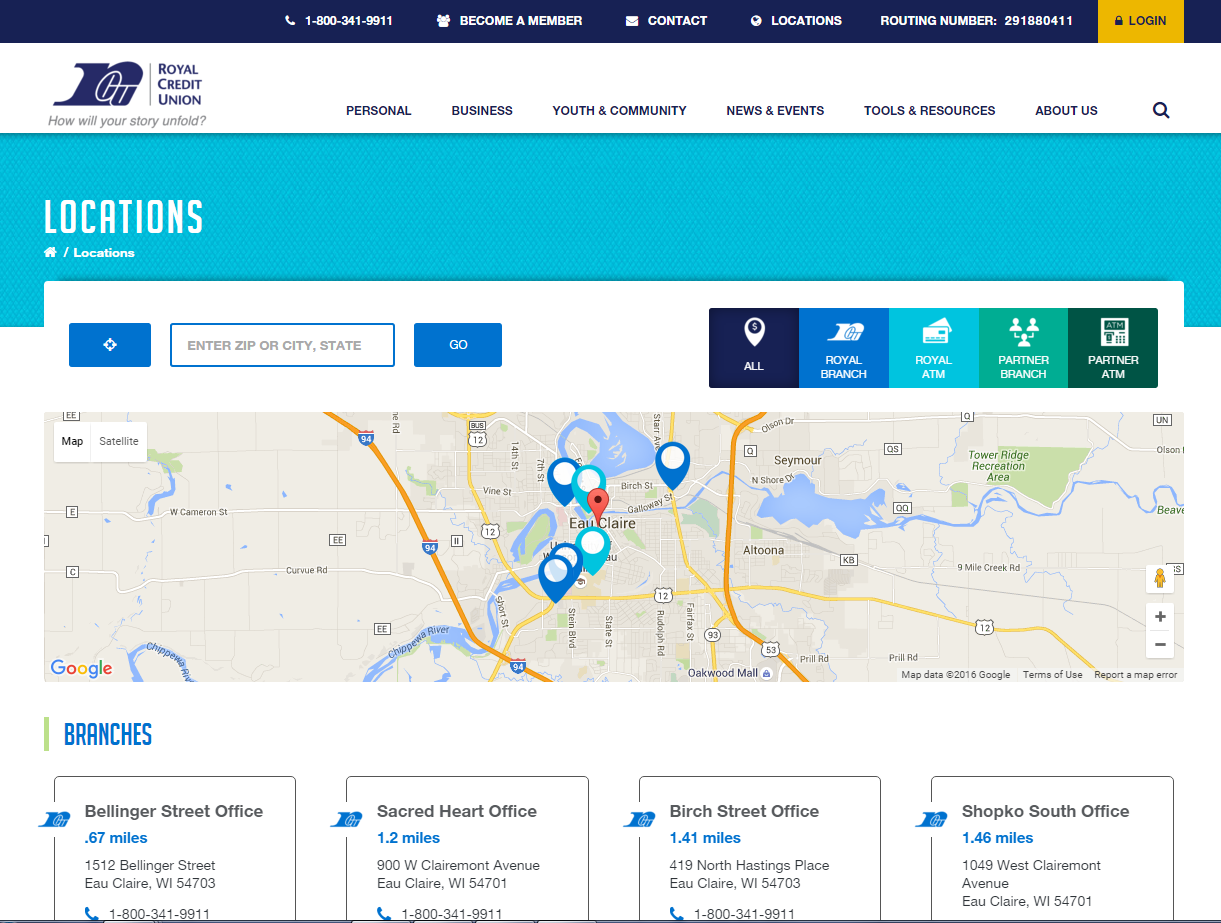

Locations & ATMs Before & After

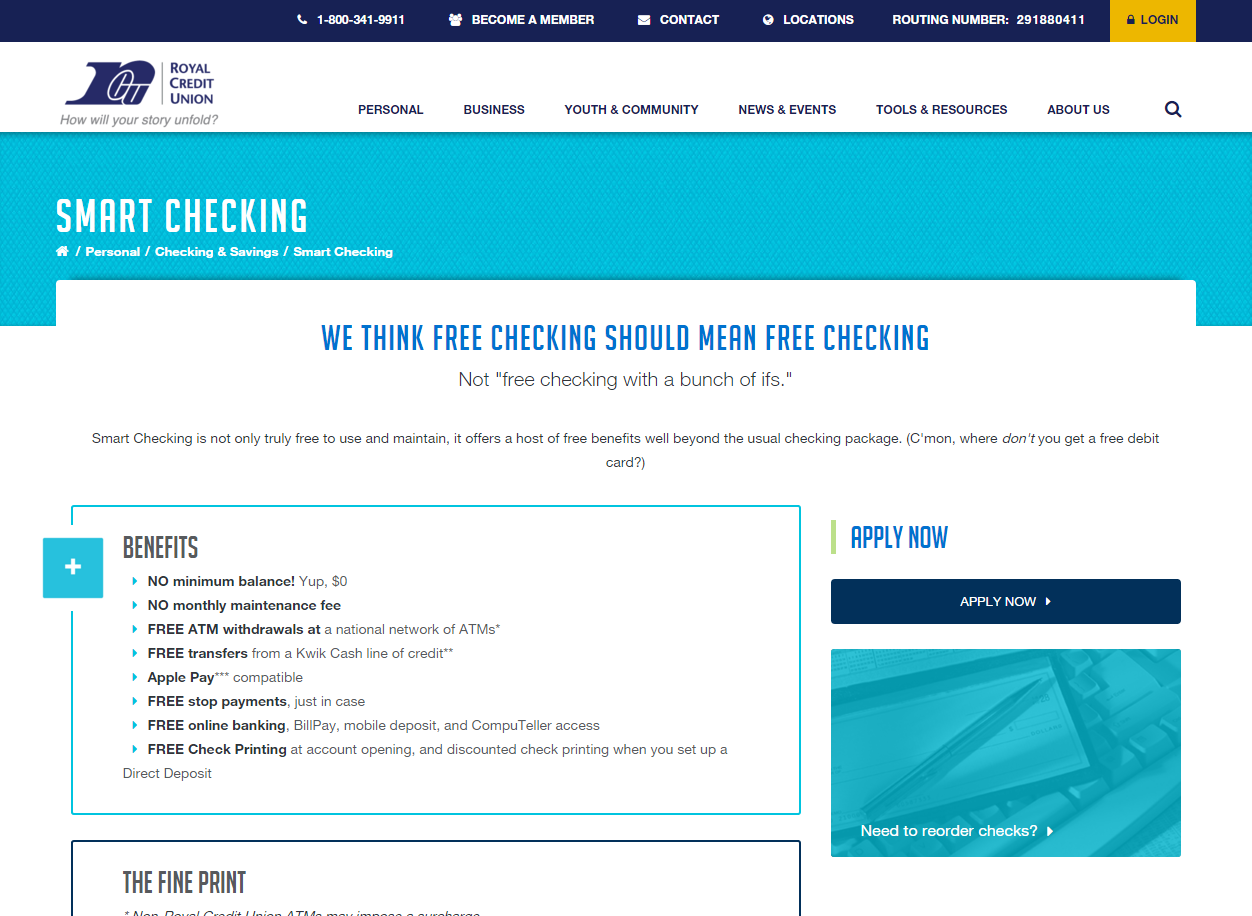

Product & Category Pages Before & After

Responsible for vendor selection, overall project management, budget management, concept, copy, navigation, design direction, and testing.

That beautiful distraction. Our phones and tablets (laptops, so recently so cool, are now becoming passe’) are getting plenty of our attention, and younger consumers in particular love the functionality available to them. From finding a pizzeria in Bangkok to finding your way home from school to finding a date for Friday night, our mobile devices have, as television ads for the Apple Store state, “an app for that.”

All told, Apple’s App Store has more than 250,000 apps, and Google’s Android platform has about 80,000. Gaming apps are most popular, followed by news, weather, social networking and music. Nearly a quarter of mobile app users have downloaded an app in the shopping or retail category.

Information impatience. With teens and young adults leading the charge, the mobile phone and app utilization trend is extremely prevalent among consumers under 35, those that fall into the oh-so-attractive-to-marketers Gens X and Y. Parks Associates, a technology research and consulting agency, discovered that these younger consumers are passing completely on laptops and desktops, and that they quickly lose patience and interest in Web sites that do not translate well on a mobile phone. (For CUs who haven’t yet optimized their sites and home banking platforms for mobile, let’s get on it!) Native mobile apps, which access content without requiring the user to access a traditional Web site (e.g., no typing in a Web address or waiting for a page to load), are highly popular.

With our attention increasingly drifting away from traditional media like television, radio – and who even has a landline phone, anyway? – some psychologists believe that we are actually reshaping our personalities. Largely, the changes are not positive, as experts assert we are becoming more impatient and impulsive.

The near-instant speed at which we can send financial reports to Singapore or find out what movies are playing at the 32-plex has conditioned us to expect everything in our lives to move just as quickly and efficiently. To illustrate, consider how irritable we become standing in grocery line; or think about the advent of road rage in rush-hour traffic.

In addition, we no longer need to research a product or service before going to a retailer; we can now do it while we’re in the brick-and-mortar business itself. About 16% of consumers reported using their mobile to compare prices (Oracle, 2011). About 10% said they have looked for more information or product reviews, and 7% reported seeking coupons or discounts.

Scientists say juggling e-mail, phone calls and other incoming information has altered our ability to patiently focus on the task at hand. The constant stimulation of the beeps, buzzes and quick responses of our mobile devices causes our brains to release dopamine, a “feel-good” brain chemical (Richtel, 2010).

Without this instant gratification, we are lost. We are bored. We need the omnipresent distraction of our mobile phones. In short, we are addicted.

Credit unions – all businesses, really – can and should capitalize on consumers’ information impatience by, first and foremost, optimizing their home banking platforms and Web sites. Clunky access is a turnoff, and will drive away potential new members. Second, everyone needs a mobile app. Third, opt-ins like promotional e-mails and text alerts give us additional member access. Finally, CUs that want to remain competitive in this brave new world absolutely need to provide convenience products like mobile deposit capture, which appeal to our increasingly impatient natures.

Let’s find ways to provide that distraction we humans have come to know, love – and need.

Why Doesn’t Anyone “Like” Us?

I work for a financial institution that boasts some 65,000 members. That’s a lot of people. Facebook has over one billion users worldwide, though, of course, most of them aren’t in my credit union’s service area. Still, I have the potential to reach about three million people in that service area, which covers Minnesota and Wisconsin. So how come we can’t even reach 700 likes on our Facebook page?

My Credit Union is on Facebook. Who Cares?

My peers in the industry struggle with the same thing: Despite diligently posting day after day, and posting what we believe is engaging content (really, it isn’t all a big sales pitch!), we can’t seem to inspire much interest. A new “like” or comment makes any CU marketing team downright giddy.

Recently, while monitoring a competing credit union’s Facebook page, I noticed they were running a costume contest, with a $50 Target gift card as the prize. I found a picture of my 1-year-old, Nate, from his first Halloween last year. I cropped it, wrote a quick caption (“I’m bananas about credit unions!”) and posted it.

We were one of only two entries, and with two “likes,” we won. I was happy about the Target gift card, but I felt kind of bad for the credit union, competitor or not.

Potential Ways Financials Can Utilize Social Media … and Maybe Even Get Some Likes!

As we move forward with our social media strategy, there are a few ways I’d like to experiment with building our “likers” base on our page. After all, what’s the point in stressing about finding the right message if nobody’s around to see it?

Here are a few ways financial services providers might get a bigger bang out of their Facebook efforts.

1. Facebook: A quasi-call center.

With larger financials like US Bank and Wells Fargo utilizing their pages as a customer service tool, it seems it will only be a matter of time before my members start thinking of Facebook before the pick up the phone and dial our call center. This is both exciting and scary. Exciting because if we do customer service well, the world can see it; and scary because if we handle a member complaint poorly, well, the same thing can happen, and the complaining member can also quickly and effortlessly shout about their experience to hundreds, if not thousands, of followers. Make sure you’ve got your A-Team handling any sort of social media customer service, so that any shares reflect well on you.

2. Plain old listening. It’s valuable.

There some very interesting conversations occurring in social media spaces. Individual users ask things like, “Got a great Thanksgiving stuffing recipe?”, yes, but they also ask things like “Where did you get your car loan?” and the answers they receive can be revealing. In addition, rants and raves occur, unfiltered. It’s like a giant focus group! Businesses, including credit unions, would be well-served to just pause between well-intentioned but ineffective posts about International Credit Union Day, and instead, snoop around. Look on other financial institutions’ pages, and, if you’re on the other platform (and you should be), try Twitter hashtags like #money. It’s the adult, modern-day equivalent of listening to the popular girls gossip while you’re locked safely in your bathroom stall.

Then, find a way to use the information you discover. Maybe you can use it for something big, like to develop a new product that would fill a need consumers are discussing. Maybe it’s simply to make your social media posts more relevant to your audience. (Once you determine what people want to know more about, financially speaking, you can post about that instead of your latest mascot appearance.)

Note: Listening in to relevant social media posts can also be done more systematically by setting up social media monitoring tools like CoTweet. (More on this in the future, because I’m looking to dig into it.)

3. A great way to do good.

The Financial Brand suggests that banks and credit unions can use the power of Facebook to build brand affinity through charitable giving campaigns.Chase recently gave away $5 million to charities via Facebook, a promotion which garnered 2,510,642 “likes” on the bank’s page. Of course, there are economies of scale at work here (few CUs could afford even a fifth of that amount), but smaller institutions could find organizations that local residents are passionate about, and build a following by offering to donate, say, $5 for every new “like” or comment. Incenting engagement and doing good? Why not?

Are Ads the Answer?

Maybe. Facebook advertising is simple, affordable, and best of all, hyper-targeted (Facebook, 2012).

Facebook’s “Marketplace Ads,” which appear on the far right of users’ main pages, can be finely targeted to our desired market segments. Using Facebook’s self-service ad creator, marketers can choose to have ads appear only to users whose profile elements match those of their target audience: geographic location, age, occupation and interests are a few.

In addition, Facebook ads, like all things Facebook, give marketers the opportunity to show off their popularity. “Likes” or “I am attending” can show up as part of the ad or event promotion itself, so when a user notices several friends have endorsed a product, even a previously uninteresting product or service suddenly becomes relevant. I know I am always curious when I see a couple of friends (or maybe especially, if a couple of rivals) have “liked” a particular brand, product or event.

Surprisingly, the medium is relatively inexpensive, and offers marketers the advantage of setting their own budget, both daily and for the life of the campaign. Through a bid system which compares an about-to-be-launched ad to similar existing ads, marketers set the price they are willing to pay per click (CPC) or per impression (CPM). Once the daily budget is met, ads simply stop appearing on any pages.

Post promotion is another new way businesses can generate attention. With Facebook’s new algorithms, users now most often see pages and people with which they have a history of interacting. This could mean more bad news for credit unions that don’t get a lot of traffic; they can fall off of news feeds entirely. To combat this, businesses can pay to promote their posts, inserting themselves onto news feeds of all of their followers, history of interest or not.

Facebook offers a reporting feature to track the efficacy of any given ad or campaign. Demographic metrics, such as the age, gender, and geographic location of the users who have clicked is readily viewable. Plus, reports can show if the ad has carried any social weight, like when an ad is viewed by someone through a Facebook friend.

One downside to advertising on the world’s most popular web site is creative limitation. Ad copy can only be 135 characters long, and ad dimensions cannot exceed 110 x 80 pixels. With short words and a small space, creative teams will need to find compelling messaging that makes less more.

With this evolving medium, I certainly don’t have all the answers; however, I plan to keep experimenting until I find a few.

Song Airlines, Delta’s now-defunct “discount airline for women,” was an attempt to build a business around a brand concept that would answer to the perceived needs and desires of the female traveler. The airline was barely off the ground – pun heartily intended – when Delta executives announced they were discontinuing Song entirely, though the trademark lime green planes would still be flying.

What went wrong? It was likely a combination of factors. First and foremost, Delta was attempting to launch a new airline brand during some of the industry’s worst-ever market conditions. From 2001 to 2004, the airline industry posted over $32 billion in losses, with at least one major carrier, US Airways, forced into bankruptcy (Morrison, 2005). It’s difficult to imagine that the leadership of an established airline like Delta was unaware of their economic environment.

Second, and of equal importance, Delta simply did not do enough broad, deliberate research at the outset of brand development. The brand fell into the dangerous territory of being too creative (the art) driven, without backing up their ideas with some solid consumer insight (the science).

PBS’s Frontline episode, The Persuaders, brought the audience behind the scenes during Song’s brand development. The creative team behind the brand conjured up Song’s ideal customer – an affluent woman with children who was concerned about things like designer labels and the “right” shoes (Frontline, 2004).

But there were problems with this model consumer – she was based on an extremely narrow demographic profile, and one largely conjured up in the minds of the creative team. There was no evidence she really existed outside of Sex and the City, and certainly not in numbers significant enough to support an entirely new airline – or that she would choose a mode of getting to point A to point B based on things like a passionfruit martini. Airline seats are largely viewed as commodities (Morrison, 2005). During brand development, the brains and imaginations behind Song did not delve deeply enough into consumers’ minds to unearth this long-held belief, and/or they overestimated their ability to make a dramatic change in the airline industry paradigm – turning a commodity into an experience.

Tim Maples, Song’s director of marketing, communicated the new airline’s intent to add emotion to an as-yet emotionless choice. He singled out JetBlue, a value carrier who has been successful not only by airline standards, but by any standards, as airline that was starting to get things, in his mind, right.

“JetBlue is a very good airline, but they left the door wide open for an airline to be better. They didn’t do as much as perhaps could be done to build a brand around a greater emotional context. Song is working hard to do that with an optimistic, can-do, up-tempo, up-beat, attitude,” said Maples (Reverie, 2004).

Song’s creative minds, laser-light focused on spreading that “attitude,” blew ahead full-bore in creating an “image” brand of air travel. They asked the New York City Meatpacking District’s bartenders to come up with a Song signature cocktail. They also opened a store for six weeks in SoHo that gave consumers a chance to purchase Song’s better-quality airline food. It generated some interest – so much so, in fact, that a similar store was launched in Boston for a short period of time. Reservations were made.

“The thought was that while there are fashion, automotive and liquor brands that have a certain badge-value, there really wasn’t an airline that reflected who people are when they fly,” said Maples, reinforcing the Song team’s unsubstantiated idea that consumers were truly looking to “express themselves” via their choice of airline.

“The Song Book,” a brand identity handbook produced by ad agency Leo Burnett and branding firm Landor Associates, lays out just what Song aims to be to the company’s executives and external marketing firms. Song is “friendly, simple, and approachable,” more like comedian Janeane Garofalo than Martha Stewart (Kirsner, 2003). The Song Book includes a “brand-inspired” CD featuring tracks by The Strokes, the Buena Vista Social Club and Portishead.

All of the creativity and brandiness would have been well and good had the Delta creative team been launching, say, a new line of ready-to-wear fashions. Women may well be the decision-makers when it comes to air travel, but, unfortunately, their buying decisions when it comes to travel are made very differently than when they make a choice to buy a new pair of Manolo Blahniks.

Because air travel has always been simply a means to a very literal end, women aren’t looking for an experience – they are primarily looking for a good value and a reasonable level of comfort. This argument is perhaps best illustrated by an action recently taken by Japan’s All Nippon Airways: In response to requests from female flyers with sensitive noses, the airline will now designating one bathroom per plane as “women only (The Telegraph, 2010).”